Types of Auto Insurance Explained (2026)

While most states require some types of car insurance, such as liability, other coverages are voluntary, such as collision. Basic coverage that meets state requirements averages $45 a month, but additional coverage raises rates. Compare different types of auto insurance to find coverage that meets your needs.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Licensed Insurance Agent

Brandon Frady has been a licensed insurance agent and insurance office manager since 2018. He has experience in ventures from retail to finance, working positions from cashier to management, but it wasn’t until Brandon started working in the insurance industry that he truly felt at home in his career. In his day-to-day interactions, he aims to live out his business philosophy in how he treats hi...

Brandon Frady

Licensed Insurance Broker

Zach Fagiano has been in the insurance industry for over 10 years, specializing in property and casualty and risk management consulting. He started out specializing in small businesses and moved up to large commercial real estate risks. During that time, he acquired property & casualty, life & health, and surplus lines brokers licenses. He’s now the Senior Vice President overseeing globa...

Zach Fagiano

Updated February 2026

https://www.4AutoInsuranceQuote.com/should-you-get-an-umbrella-policy-if-you-already-have-auto-insurance/

https://www.4AutoInsuranceQuote.com/should-you-get-an-umbrella-policy-if-you-already-have-auto-insurance/

- The most common types of auto insurance include liability, collision, comprehensive, personal injury protection (PIP), MedPay, and uninsured/underinsured motorist coverage

- Other auto insurance coverage types include rental reimbursement, gap coverage, roadside assistance, and mechanical breakdown insurance

- Full coverage insurance is a combination of coverage types that protect from various losses

Auto insurance is a must for anyone who owns or drives a car. It helps protect you from financial risk and offers peace of mind in case of an accident.

Depending on your state, the minimum auto insurance coverage you need will vary. To ensure you are well protected, you should know the different types of auto insurance coverage.

This guide will explain the different types of auto insurance and what auto insurance does so you can determine the coverage you need.

Most Common Types of Auto Insurance

There are several types of car insurance coverage available to meet your needs. Here are some of the most common:

- Types of Auto Insurance Coverage

- Affordable Uninsured or Underinsured Auto Insurance Coverage (2026)

- Affordable Collision Auto Insurance Coverage (2026)

- Can I get auto insurance for a car that is used for towing or hauling?

- Can I get auto insurance for a car that is used for teaching or driver education purposes?

- Can I get auto insurance for a car that is used for business purposes?

- What is gap insurance and do I need it when filing an auto insurance claim?

- Get Affordable Postmates Auto Insurance Quotes (2026)

- Affordable Guaranteed Auto Protection (GAP) Insurance Coverage (2026)

- Get Affordable Delivery Driver Auto Insurance Quotes (2026)

- Affordable Comprehensive Auto Insurance Coverage (2026)

- Affordable Personal Injury Protection (PIP) Auto Insurance Coverage (2026)

- Affordable Full Coverage Auto Insurance (2026)

- Cheap Auto Insurance for Pizza Hut Delivery Drivers in 2026 (10 Most Affordable Companies)

- Get Affordable Papa John’s Auto Insurance Quotes (2026)

- Get Affordable Pizza Delivery Driver Auto Insurance Quotes (2026)

- Understanding How Auto Insurance Works (2026)

- How To Insure Aftermarket Parts On Your Vehicle (2026)

- Cheap Non-Owner SR22 Insurance in 2026 (10 Most Affordable Companies)

- Combining Insurance Policies

- Collateral Protection Insurance (CPI) 2026

- Affordable SR-50 Auto Insurance (2026)

- FR-44 Auto Insurance Explained (2026)

- Comprehensive vs. Collision Auto Insurance Coverage in 2026 (Differences Explained)

- Best Full-Glass Coverage Auto Insurance in 2026 (Find the Top 10 Companies Here!)

- Self-Insured Auto Insurance: An Affordable Alternative (2026)

- Pleasure Use vs Commuter Auto Insurance in 2026 (Differences Explained)

- Cheap One-Day Auto Insurance in 2026 (Compare the Top 10 Companies)

- Best Temporary Auto Insurance in 2026 (Find the Top 10 Companies Here!)

- Best Fleet Vehicle Auto Insurance in 2026 (Your Guide to the Top 10 Companies)

- Affordable Property Damage Liability (PDL) Auto Insurance Coverage (2026)

- Affordable Roadside Assistance Coverage (2026)

- Affordable SR-22 Auto Insurance (2026)

- Affordable Non-Owner Auto Insurance Coverage (2026)

- Liability Auto Insurance in 2026 (See Rates & Exclusions Here!)

- Affordable No-Down-Payment Auto Insurance (2026)

- Affordable Monthly Auto Insurance (2026)

- Car Insurance Classification Groups

- Does auto insurance cover hurricane damage?

- Affordable Auto Insurance for Rideshare Drivers

- Liability auto insurance

- Collision car insurance

- Comprehensive car insurance

- Uninsured/Underinsured motorist coverage

- Personal Injury Protection (PIP)

- MedPay Coverage

Most states require drivers to carry at least a minimum amount of liability coverage and may require other coverage, such as uninsured motorists. The average cost of basic auto insurance is $45 a month.

However, many drivers choose to carry full coverage, which includes any state-mandated coverage as well as collision and comprehensive. Full coverage averages $119 a month. So, your coverage amount helps determine your rates.

Continue reading to find out more about each type of coverage.

Liability Auto Insurance

Liability auto insurance is the most basic type of car insurance required by most states. It financially protects you from damages you cause in an at-fault accident. It pays for any damage you cause to another person’s body, property, or personal belongings.

While it won’t cover medical or auto repair expenses for you or your passengers, it can provide financial protection if someone sues you following an accident.

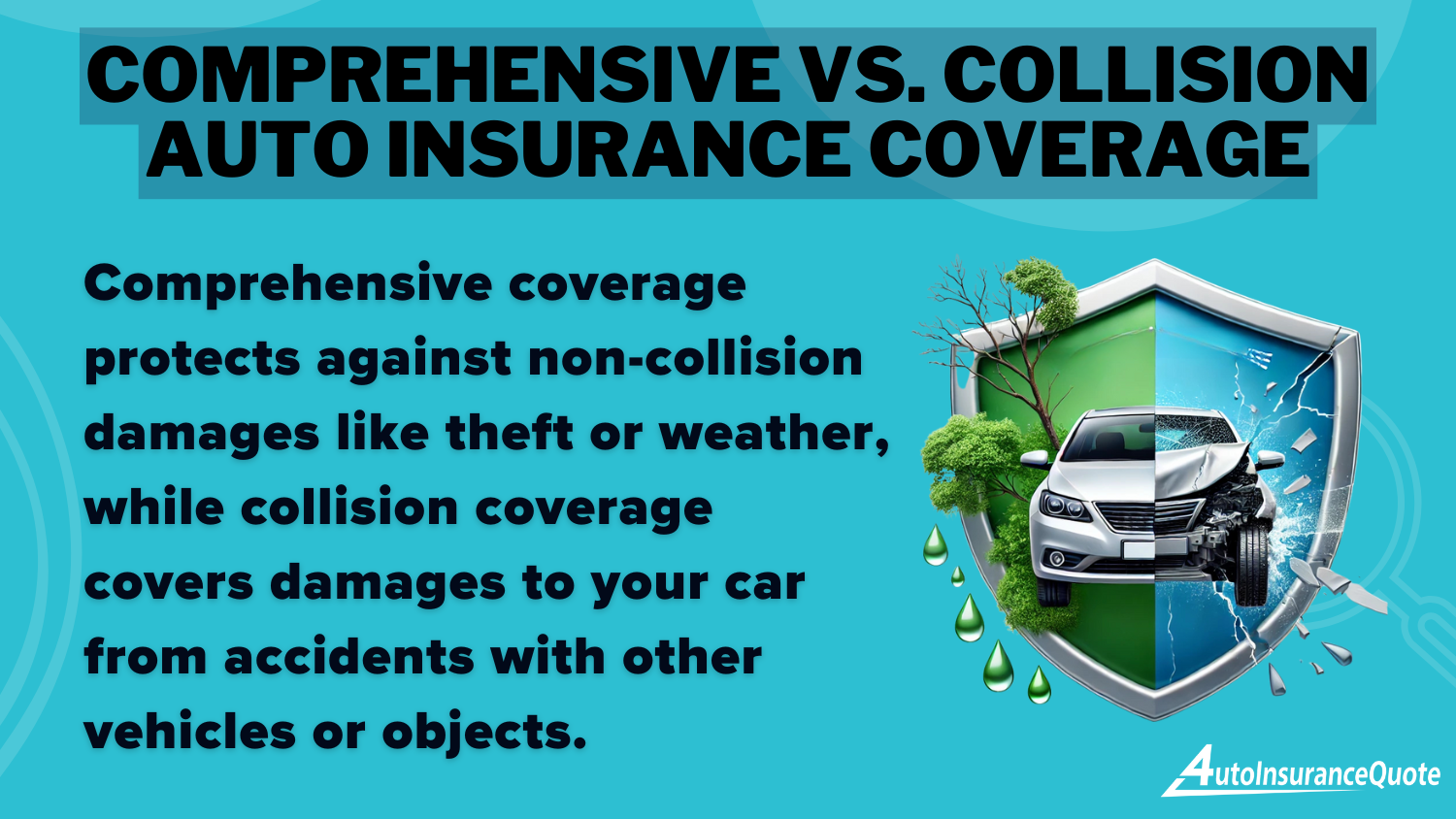

Collision Auto Insurance

Regardless of who was at fault in an accident, collision coverage assists in paying for repairs to your car. Collision insurance protects your car from damage caused by:

- An accident with another vehicle

- An accident with an object (e.g., a tree or a sign)

- An accident with a driver with inadequate insurance coverage

Collision coverage pays out based on how much your car is worth on the market right now, less any deductible. This coverage is optional in many states, but most lenders will require it if you finance or lease a car.

Comprehensive Auto Insurance

Comprehensive auto insurance protects you from losses that aren’t the result of a collision with another vehicle. Again, if you are leasing or financing your car, your lender will likely require you to have full coverage with collision and comprehensive auto insurance.

Comprehensive auto insurance covers:

- Weather-related damage (such as hail or flooding),

- Theft

- Vandalism

- Fire

It also covers any damage to your vehicle caused by an animal or a falling object, such as a tree branch.

Read more: Does my auto insurance cover damage caused by a deer or other wildlife?

Even if you own your car outright, getting comprehensive coverage is a good idea, especially if you live in an area prone to extreme weather (such as hurricanes). Comprehensive coverage can provide extra peace of mind that your vehicle will be covered in storm-related damage.

Read more:

- Does my auto insurance cover damage caused by a flood or hurricane?

- Does auto insurance cover hurricane damage?

It’s important to note that while comprehensive coverage does provide wide-ranging protection against many different types of losses, it does not cover all potential damages.

For example, it does not cover the repair costs associated with an accident involving another vehicle, collisions with property, or multi-car accidents

Uninsured/Underinsured Motorist Coverage

Suppose you are involved in an accident with someone with little or no insurance coverage. In that case, uninsured or underinsured motorist coverage can help protect you from financial losses.

This type of insurance pays for your medical bills and other damages if you get into an accident with a driver without insurance or insufficient insurance. Learn more about what happens if you hit an uninsured driver.

It is important to note that uninsured motorist coverage is a legal requirement in 20 states, including California and New York. If you live in one of these states and do not have this coverage, you may be subject to fines or other penalties.

Personal Injury Protection (PIP)

Personal Injury Protection (PIP) is a type of no-fault car insurance that helps cover medical bills, lost wages, and other expenses after an auto accident. It can also help cover the costs associated with funeral services in the event of a death.

PIP coverage pays regardless of who is at fault in a crash, so you don’t have to worry about lengthy lawsuits or expensive court battles for coverage if you’re hurt in an accident. Depending on your policy limits, PIP can provide up to $10,000 worth of coverage per person.

PIP coverage is mandatory in 12 states, including New York and Florida. In other states, it is optional but highly recommended, as it can save you thousands of dollars in medical expenses in the event of an accident.

Although PIP insurance provides much coverage, it does not cover certain injuries and activities.

For example, PIP does not cover farm equipment, recreational or off-road vehicles, mopeds, or motorcycles. Some motorcycle insurance policies may include PIP coverage but are usually very expensive.

PIP will also not cover injuries resulting from intentional acts by the insured person or if they become injured while participating in organized racing activities or committing a felony.

Medical Payments (MedPay) Coverage

Let’s say you want extra coverage to help pay for your medical bills after a car accident. In such a case, MedPay coverage may be a good option. MedPay, or medical payments coverage, helps pay for accident-related medical expenses for you, your passengers, and other policyholders.

MedPay is required in Maine and New Hampshire but is optional in all other states.

This type of auto insurance is similar to PIP coverage but with a narrower scope. Nonetheless, MedPay coverage is usually a worthwhile investment as it can provide vital financial support in the event of an accident.

Since the average bodily injury claim after a car accident can reach over $20,235, having MedPay insurance can help cover any medical expenses that might not be covered by health insurance or personal injury protection (PIP).

Read more: Does my auto insurance cover my medical expenses after an accident?

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Optional Types of Auto Insurance Coverage

In addition to the previously mentioned types of car insurance coverage, other coverages are available depending on your state and insurer. These include:

Gap Insurance

Gap insurance covers the difference between the amount of money owed on an auto loan and the actual cash value of the vehicle if it’s totaled or stolen.

It is essential for those financing or leasing their vehicles since this insurance will help you recover any financial losses in such circumstances. Learn how much gap insurance costs.

Umbrella Insurance

Umbrella insurance provides additional liability coverage beyond the limits of your auto and home insurance policies. In addition, it covers situations like major accidents and lawsuits from third parties and things that regular auto insurance may not cover. (For more information, read our “Affordable Umbrella Auto Insurance Coverage”).

Read our guide to find out when you Should you get an umbrella insurance policy if you already have auto insurance?

SR-22 Insurance

SR-22 insurance is required for drivers who were convicted of certain violations, such as driving under the influence (DUI) or having multiple traffic violations within a certain time frame. You may also need to file SR-22 if you’re involved in serious at-fault accidents without proper auto liability limits or had your license revoked.

SR-22 forms aren’t actual insurance coverage but prove that you have the minimum required car insurance in your state. Learn more in our SR-22 auto insurance guide.

Rental Reimbursement

Rental reimbursement coverage reimburses you for transportation expenses when your vehicle is out of commission due to an accident or other covered event. For example, this may cover the cost of renting a car or rideshare services while yours is being repaired.

Mechanical Breakdown Insurance

Mechanical breakdown insurance helps cover the costs of breakdowns after your manufacturer’s warranty has ended or when your vehicle warranty doesn’t cover a mechanical failure.

Emergency Roadside Assistance

Emergency roadside assistance typically includes tow truck services, flat tire changes, jump-starts, refills of gas/fluids, locksmith services, and extrication services necessary due to an accident or breakdown.

Non-Owner Auto Insurance

Non-owner car insurance provides liability coverage for those who don’t own a car but still want basic liability coverage. It’s useful if they get into an accident while driving someone else’s vehicle or renting a car on occasion.

Usage-Based Insurance (UBI)

This new way to pay for car insurance uses sensors and telematic technology to track your driving habits. It rewards safe drivers with discounted rates based on their driving habits.

Classic Car Insurance

Classic car insurance is for vehicles considered ‘collector’s items’ and driven infrequently (read our “When is a car considered a classic?” for more information. Therefore, it typically offers coverage more specific to these vehicles than regular auto insurance.

How to Buy the Right Type of Auto Insurance

Now that you understand the different types of car insurance coverage available, here are some tips to help you choose the right policy:

- Know what type of coverage you need. Do you need liability only, or do you require more extensive coverage such as comprehensive and collision?

- Decide how much insurance coverage you need. How much coverage you need depends on your age, ZIP code, and vehicle make and model.

- Shop around. Shop around and compare auto insurance coverage types from several insurers to get the best rate. Companies may offer discounts and coverage options, so it pays to shop around.

- Ask about discounts. Ask your insurer if they offer discounts such as multi-car, good driver discounts, or low mileage discounts. Check the company’s website to see if they list any discounts.

- Read the policy carefully. Read your policy carefully and ensure you understand what’s covered and what’s not.

There is more than one way to get affordable auto insurance rates — find out the top 10 secrets for getting cheap car insurance.

The Bottom Line on the Different Types of Auto Insurance Coverage

Auto insurance is an important financial safety net for drivers and their families. Therefore, you should understand the different types of car insurance coverage available to ensure you are protected in the event of an accident.

Liability, collision, comprehensive, personal injury protection (PIP), MedPay, and uninsured/underinsured motorist coverage are the six main auto insurance coverage types.

Read more:

- Can I get auto insurance for a car that is used for teaching or driver education purposes?

- Affordable Non-Owner SR-22 Insurance

Other coverages are available depending on the state and insurer, such as gap insurance, umbrella insurance, SR -22 insurance, rental reimbursement, mechanical breakdown insurance, emergency roadside assistance, and non-owner car insurance.

Take your time to shop for the best car insurance rate and coverage types that suit your needs.

Read more: Car Insurance Classification Groups

Frequently Asked Questions

How does auto insurance work?

You know that you need insurance, but what does car insurance do? Auto insurance is a type of coverage that helps to protect drivers and their vehicles in the event of an accident or other covered loss. It can cover the damages to vehicles, liability for injuries, and other expenses related to an accident.

Does insurance cover hit and run?

Hit-and-run accidents are typically covered under your collision coverage if you have it. Liability insurance does not cover hit-and-run accidents because the at-fault party is not identified. Your uninsured/underinsured motorist coverage may cover your losses if you can identify the at-fault driver and they do not have enough insurance.

What does auto insurance cover?

Car insurance covers various expenses, including medical expenses, repair costs for damaged vehicles, liability for injuries, and legal fees. It depends on the policy and coverage types that you have.

Liability, collision, comprehensive, personal injury protection (PIP), MedPay, and uninsured/underinsured motorist coverage are the most common types of car insurance coverage.

What is full coverage insurance?

Full coverage insurance is a term used to describe a combination of coverage types that protect from losses due to accidents and other covered risks. It typically includes liability, collision, comprehensive, and uninsured/underinsured motorist coverage.

What is collision coverage on a car?

Collision coverage is a type of auto insurance coverage that helps to pay for damages to your vehicle if you are in an accident with another car or object. It pays for repairs to your vehicle regardless of who is at fault in the accident.

Is comprehensive insurance the same as full coverage?

No, comprehensive insurance is not the same as full coverage. Comprehensive insurance covers losses to your vehicle caused by non-accident-related events, such as theft, fire, or weather-related damage. Full coverage insurance is a combination of coverage types that protect from various losses.

What are the five types of auto insurance?

The five main types of auto insurance are liability, collision, comprehensive, personal injury protection (PIP), and uninsured/underinsured motorist coverage.

What is the most common car insurance?

The most common type of car insurance is liability coverage. This covers expenses related to damage to other people and property caused by you while driving your vehicle. Liability coverage is a legal requirement in most states.

Is comprehensive insurance worth it on an older car?

If the cost of premiums exceeds the car’s value, comprehensive insurance may not be worth it. On the other hand, if the cost of premiums is low compared to the car’s value, comprehensive insurance may be something to think about.

Related Articles

-

Jun 2024

Does auto insurance cover a DUI accident?

-

Jan 2024

Affordable High-Risk Auto Insurance (2026)

-

Nov 2024

Comprehensive vs. Collision Auto Insurance Coverage in 2026 (Differences Explained)

-

Dec 2023

How To Renew Your Auto Insurance Policy (2026)

-

Feb 2025

Does my auto insurance cover damage caused by a runaway vehicle?

-

Nov 2024

Affordable SR-50 Auto Insurance (2026)

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.