What an Auto Insurance Policy Looks Like

What does an auto insurance policy look like? An insurance policy looks like an identification card. Drivers can carry paper copies on their person or in their vehicles, or access digital copies from their provider's mobile app. Your insurance policy will list the kind of coverage you have as well as your coverage limits. A car insurance policy is required in almost every state, and you will need to show proof of insurance in order to buy and register a new vehicle.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Farmers CSR for 4 Years

Leslie Kasperowicz holds a BA in Social Sciences from the University of Winnipeg. She spent several years as a Farmers Insurance CSR, gaining a solid understanding of insurance products including home, life, auto, and commercial and working directly with insurance customers to understand their needs. She has since used that knowledge in her more than ten years as a writer, largely in the insurance...

Leslie Kasperowicz

Licensed Insurance Agent

Eric Stauffer is an insurance agent and banker-turned-consumer advocate. His priority is educating individuals and families about the different types of insurance coverage. He is passionate about helping consumers find the best coverage for their budgets and personal needs. Eric is the CEO of C Street Media, a full-service marketing firm and the co-founder of ProperCents.com, a financial educat...

Eric Stauffer

Updated March 2025

Auto insurance is required by law in all 50 states, and for a good reason too. Auto insurance protects a car and its owner from the unthinkable. Although extremely important, it’s also very complicated. With hundreds of different options available to insure a car, it’s not surprising that it confuses many consumers.

Insurance, by definition, is an agreement between a person and an insurance provider in which the person pays the provider money in exchange for protection from financial losses. In other words, you pay your insurance company for financial security. Auto insurance, for example, protects people in case of accidents with their vehicle.

We need auto insurance because driving is dangerous. Whenever we get behind the wheel of our vehicles, there is a chance we will do damage to our car, other cars, ourselves, or other people. These expenses can be costly. Most people don’t have nearly enough money to pay for them. This is why car insurance is needed and required by law.

Types Of Insurance Coverage In A Policy

Auto insurance policies contain several different types of coverages. Required coverages vary state by state. All states, however, require something known as “liability insurance.” Liability insurance covers you in case you do damage to other vehicles. In the event of an accident, liability insurance will pay for the other party’s car damage, bodily injury, and property damage. It does not cover damage to your vehicle or property, only to other people’s. The reason liability insurance is required is because it’s the government’s job to protect its citizens. Requiring liability insurance by law is a way to make sure people are protected from damage caused by others.

So, in the United States, all auto insurance policies must include liability insurance, but what other types of insurance might be included? Let’s take a look:

Additional Types Of Insurance Coverage

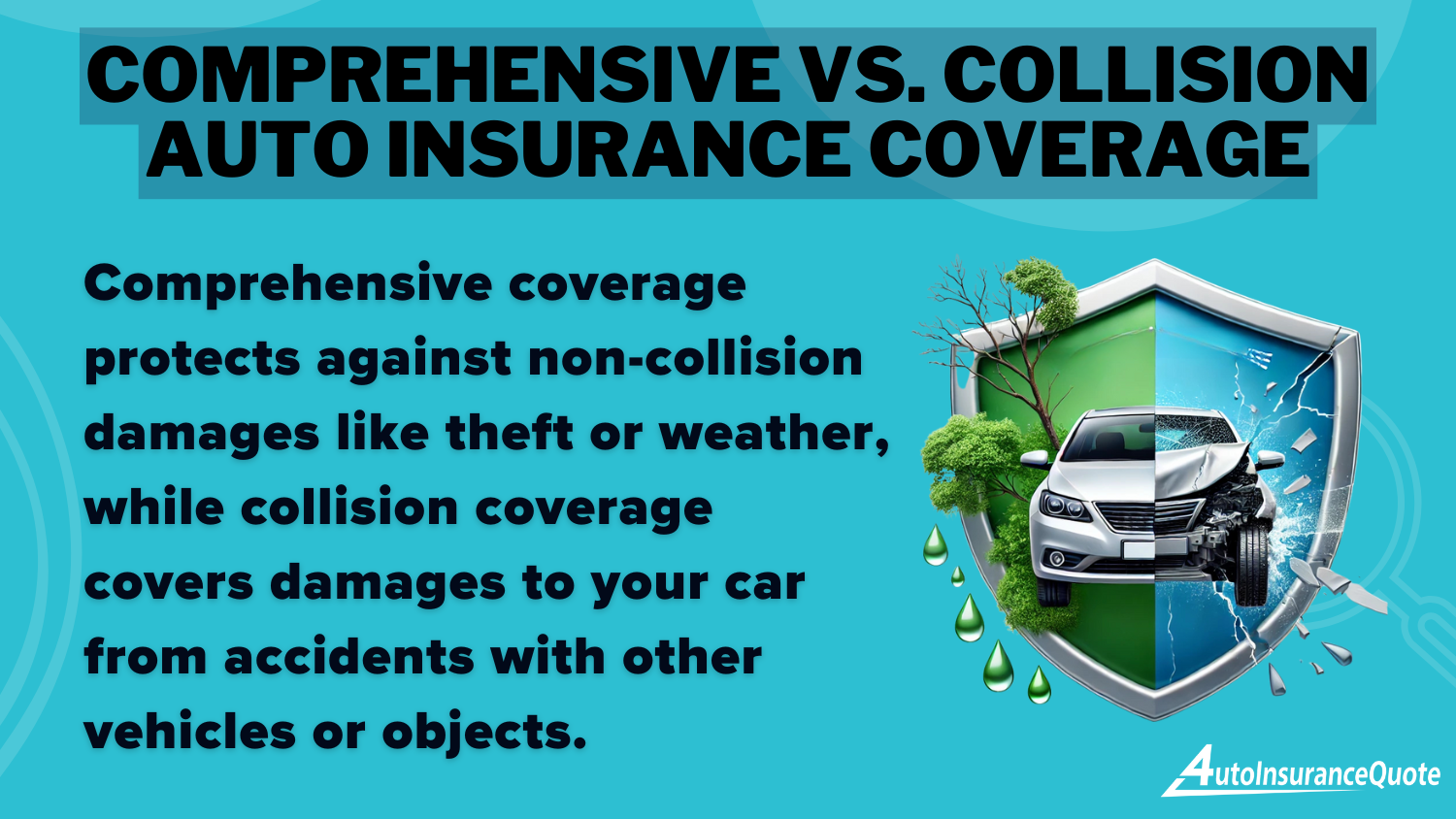

Collision coverage is one of the most popular coverage types. Like stated above, liability insurance covers damage you might cause to others. Collision coverage, on the other hand, protects your vehicle. If you are ever in an accident and your vehicle is scratched, dented, flattened, or totaled, collision coverage will pay for it to be repaired or replaced. If you have an old car that is not worth much money, it might not be in your best interests to get collision coverage.

Comprehensive coverage is another popular type of coverage. It will cover damages caused by anything but collisions. This includes theft, vandalism, and natural disasters (fire, snow, hurricanes, etc.). If you live in a safe, calm area, you might consider dropping or not purchasing comprehensive coverage.

Uninsured and under-insured motorist coverage protects you in case the driver of the other vehicle hits you and does not have adequate insurance. Although liability insurance is required by law, that does not mean everybody has it. Many people take the considerable risk of driving without insurance and end up paying gravely for it (license suspension and incarceration are just some of the consequences of driving without insurance). If you are involved in an accident and the at-fault driver does not have insurance, it could be quite challenging to pry money from him/her. This is where uninsured or under-insured motorist comes in. It will protect you in situations such as this.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Insurance Policy Limits

Now that you are familiar with the coverage types, you should also familiarize yourself with limits. On your insurance policy, you might see a group of numbers that look like this: 200/400/250, Deductibles: 700 / 700. If you don’t know what this means, don’t worry, I’ll decode it for you:

- 200 = $200,000 of Bodily Injury Coverage per Person in an Accident

- 400 = $400,000 of Bodily Injury Coverage for all Persons in an Accident

- 250 = $250,000 of Liability Property Coverage per Accident

- 700 = $700 Comprehensive Deductible

- 700 = $700 Collision Deductible

These numbers represent the amount of money your insurance company will pay out to you in the event of an accident. The more money you pay for insurance, the more coverage you will have. To determine how much coverage you need, it’s best to analyze your individual situation.

Choosing The Right Insurance Policy For You

Before choosing your insurance coverage, it’s best to understand your needs and wants. Once you know what type of coverage you need, then you can shop around and get quotes from different companies. It is highly recommended to compare rates to get the best premium for you and your family. (Note – a premium is the price of all coverage types included in your policy.) If you are ready to start comparing quotes, go to the top of this page and enter your zip code. Your journey to low premiums begins now.

Frequently Asked Questions

What does an auto insurance policy look like?

An auto insurance policy looks like an identification card that lists the coverage types and limits. It can be a physical copy or accessed digitally through the insurer’s mobile app. Proof of insurance is required to buy and register a new vehicle.

Why do I need auto insurance?

Auto insurance is required by law in almost every state because driving can be risky. It provides financial protection in case of accidents or damage to your vehicle, other vehicles, or people. Most people don’t have enough money to cover these expenses on their own.

What types of coverage are included in an auto insurance policy?

Auto insurance policies typically include liability insurance, which covers damages to other vehicles and injuries to others. Additional coverage options may include collision coverage for your vehicle’s damage and comprehensive coverage for non-collision incidents like theft or natural disasters.

What do the numbers on my insurance policy mean?

The numbers on your insurance policy represent the coverage limits. For example, “200/400/250” may indicate that your liability insurance will pay up to $200,000 for bodily injury per person, $400,000 for bodily injury per accident, and $250,000 for property damage. Deductibles are separate and indicate the amount you must pay out of pocket before the insurance kicks in.

How can I choose the right insurance policy for me?

It’s essential to assess your needs and wants regarding coverage types and limits. By comparing quotes from different insurance companies, you can find the best premium that suits your requirements. Use online tools or enter your ZIP code to start comparing quotes and find the most suitable coverage for you and your family.

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.