Can I get backdated auto insurance?

If you are wondering can I get backdated auto insurance, the answer is that backdated auto insurance is usually not permitted by auto insurance companies. In some circumstances, backdating auto insurance may even be considered insurance fraud, which can come with serious criminal penalties.

Read more![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Published Insurance Expert

Melanie Musson is the fourth generation in her family to work in the insurance industry. She grew up with insurance talk as part of her everyday conversation and has studied to gain an in-depth knowledge of state-specific insurance laws and dynamics as well as a broad understanding of how insurance fits into every person’s life, from budgets to coverage levels. Through her years working in th...

Melanie Musson

Licensed Insurance Agent

Michelle Robbins has been a licensed insurance agent for over 13 years. Her career began in the real estate industry, supporting local realtors with title Insurance. After several years, Michelle shifted to real estate home warranty insurance, where she managed a territory of over 100 miles of real estate professionals. Later, Agent Robbins obtained more licensing and experience serving families a...

Michelle Robbins

Updated November 2024

- In 2017, the number of auto accidents was more than 6 million, with two years prior reporting 13 percent of drivers were not insured.

- The average amount of uninsured/underinsured driver coverage was in the $25,000 to $50,000 range.

Can I get backdated auto insurance? The answer is that backdated auto insurance is tricky. It’s a legal requirement in most states for all drivers to have auto insurance to cover the costs of any damage they cause in an accident.

If you don’t have insurance during an accident, it will be very hard to backdate insurance. Read on to learn everything you need to know about understanding auto insurance and backdating.

Before learning more about getting backdated car insurance, enter your ZIP code into our free quote tool to find affordable auto insurance in your area to insure you never have a lapse in coverage.

Understanding Backdated Insurance: Risks and Realities

Backdating insurance refers to the practice of setting the effective date of an insurance policy to a past date. This can apply to various types of insurance, including auto insurance.

However, backdating car insurance is generally not allowed due to the potential for fraud and financial risk to insurance companies. Understanding the implications and legalities of backdated insurance coverage is crucial for all drivers.

Common Scenarios for Backdating Insurance

While backdating insurance coverage is rarely permitted, some individuals may seek it under certain circumstances:

- Accidental Lapses: Drivers who unintentionally let their policy lapse may look to backdate insurance to cover the gap. For instance, obtaining auto insurance after lapse is crucial to avoid penalties and higher future premiums.

- Immediate Needs: If someone needs immediate coverage due to an oversight or administrative error, they might inquire about same day auto insurance or retroactive auto insurance.

Risks of Backdating Car Insurance

Attempting to backdate insurance policies, such as a backdated insurance card or backdated insurance coverage, can lead to severe consequences:

- Fraud Accusations: Backdating insurance policy coverage, including car insurance back date or backdate car insurance policy, is often considered fraudulent. This can lead to criminal charges and hefty fines.

- Financial Penalties: Insurance companies that back date policies are rare, and those found attempting this could face significant financial repercussions, including increased premiums and the cost of claims out-of-pocket.

- Legal Issues: Backdating auto insurance policies, such as backdating car insurance cancellation or backdating in insurance, can result in legal trouble. In Pennsylvania, an insurer may backdate under specific conditions, but this is not the norm.

Alternatives to Backdating Insurance

For those experiencing a lapse in coverage, exploring legitimate options is essential:

- Reinstatement: Many insurers offer a grace period for policy reinstatement. For example, Liberty Mutual backdate the cancellation policies can sometimes be adjusted to accommodate short lapses without backdating.

- Temporary Coverage: Progressive temporary car insurance or Geico non-owner car insurance can be useful for those needing short-term solutions. This helps maintain coverage without the need for backdating.

- Specialized Policies: SR22 insurance VA no car or non-owner car insurance Geico are options for those needing specific coverage types due to legal requirements or unique circumstances.

Affordable Auto Insurance Solutions

Finding affordable auto insurance is a priority, especially after a lapse. Options include:

- Comparison Shopping: Using tools to compare quotes from multiple providers can help find the best car insurance after a lapse in coverage. This can ensure you get a car insurance low quote without compromising on coverage.

- Regional Options: For instance, Affordable Auto Insurance in Michigan or cheap auto insurance reading PA can offer localized solutions that are both comprehensive and cost-effective.

While the temptation to backdate insurance coverage might arise, the risks far outweigh the benefits. It’s essential to maintain active auto insurance and explore legitimate avenues for coverage if a lapse occurs.

Remember, backdating insurance policy coverage or seeking a backdated insurance policy can lead to severe legal and financial consequences. Always strive for continuous coverage and consult with reputable insurance providers to find solutions that fit your needs without resorting to backdating.

What does it mean to backdate your auto insurance policy?

The concept of backdating insurance is a simple one. Basically, the idea is that you would purchase insurance for a date in the past. For some situations, this is relatively benign, such as backdating coverage to prevent a gap in your insurance. There are many dangers of letting your auto insurance lapse.

Other situations aren’t so simple, such as attempting to backdate coverage because you got into an accident without insurance.

In the vast majority of cases, insurance companies will not allow you to backdate your auto insurance policy.

Insurance policies almost always go into effect on the date of purchase, though it is also possible to buy a policy before you need it and request that it go into effect on a specific date in the future. A backdated auto insurance policy is rare.

Why would I need my auto insurance backdated?

There are a few different scenarios where an individual might find themselves needing backdated auto insurance. For example, if you find that your previous policy expired but you were not aware of it, then you might want to take out insurance to prevent having a gap in coverage.

Or perhaps you purchased a used car directly from another person rather than a dealership and you were in an accident before you added the car to your policy.

So in these circumstances, what can you do? Can auto insurance be backdated?

Can I backdate auto insurance?

Unfortunately, the answer is usually no. While it would be very useful for the driver and the victim of an accident to be able to get backdated insurance, the problem is that this would in no way benefit the auto insurance companies.

Why won’t auto insurance companies agree to backdate policies?

Auto insurance companies need to make money just like any other business, which means they calculate your rates very carefully to make sure they are taking in more than they are paying out so that losses for the insurance company don’t occur.

The fewer accidents insurance companies pay for, the greater their profit margins are likely to be. This is why it’s often easier to get cheaper auto insurance if you have a clean driving record.

Getting insurance right after an accident and backdating it so you were covered during that time means you’re guaranteeing the company will have to pay a claim.

It isn’t just the start date of your insurance policy you need to worry about, either. Most insurance companies also will not allow backdating insurance cancellations because you’re paying for coverage during a specific period of time, regardless of whether or not you file a claim.

What are the legal issues with backdated auto insurance?

There are also legal issues with backdating insurance. Keep reading for more.

Why do you need continuous auto insurance on your vehicle?

The whole idea of insurance is to make drivers safer on the road by giving them the financial ability to pay for damages in an accident. Because of the importance of being financially responsible for any damage you cause, driving without auto insurance is illegal.

This table shows the penalties for driving without insurance by state.

Penalties for Driving Without Auto Insurance by State| States | Penalties |

|---|---|

| Alabama | Up to $500, Registration suspension with $200 reinstatement fee |

| Alaska | License suspension for 90 days |

| Arizona | $500 (or more), License/registration/license plate suspension for three months |

| Arkansas | $50 to $250, Suspended registration/no plates until proof of car insurance coverage plus $20 reinstatement fee; court may order impoundment |

| California | $100-$200 plus penalty assessments, Court may order impoundment |

| Colorado | $500 minimum fine, 4 points against your license; license suspension until you can show proof to the DMV that you are insured. Courts may add up to 40 hours community service |

| Connecticut | $100-$1000, Suspended registration/license for one month (show proof of insurance) with $175 reinstatement fee |

| Delaware | $1,500 minimum fine, License/privilege suspension for six months |

| Florida | Suspension of license and registration until reinstatement fee is paid and non-cancelable coverage is secured; $150 fee for first reinstatement |

| Georgia | Suspended registration with $25 lapse fee and $60 reinstatement fee. Pay any other registration fees and vehicle ad valorem taxes due |

| Hawaii | $500 fine or community service granted by judge, Either license suspension for three months or a required nonrefundable car insurance policy in force for six months |

| Idaho | $75, License suspension until financial proof. No reinstatement fee. |

| Illinois | $500 minimum, License plate suspension until $100 reinstatement fee and insurance proof |

| Indiana | License/registration suspension for 90 days to one year |

| Iowa | $500 if in accident; Otherwise, fine: $250, Community service in lieu of fine. Possible citation/warning if pulled over plus removal of plates and registration possible when pulled over without insurance and reissued upon payment of fine or completed community service, proof of insurance, and $15 fee; possible impoundment when pulled over |

| Kansas | $300 to $1,000, Fine and/or confinement in jail up to six months; license/registration suspension; reinstatement fee: $100 |

| Kentucky | $500 to $1,000, Fine and/or sentenced up to 90 days in jail; license plates and registration revoked for one year or until proof of insurance is shown |

| Louisiana | $500 to $1,000, If in car accident, fine plus registration revoked and driving privileges suspended for 180 days |

| Maine | $100 to $500, Suspension of license and registration until proof of insurance |

| Maryland | Lose license plates and motor vehicle registration privileges; pay uninsured motorist penalty fees for each lapse of insurance — $150 for the first 30 days, $7 for each day thereafter; Pay a restoration fee of up to $25 for a vehicle's registration |

| Massachusetts | $500 to $5,000, Fine and/or imprisonment for one year or less |

| Michigan | $200 to $500, Fine and/or imprisonment for one year or less; license suspension for 30 days or until proof of insurance; $25 service fee to Secretary of State |

| Minnesota | $200 to $1,000, Fine (or community service) and/or imprisonment for up to 90 days; License and registration revoked for no more than 12 months |

| Mississippi | $1,000, Driving privileges suspended for one year or until proof of insurance |

| Missouri | Four points against driving record; driver may be supervised; suspended until proof of insurance with $20 reinstatement fee |

| Montana | $250 to $500, Fine and/or imprisonment for no more than 10 days |

| Nebraska | License and registration suspension; reinstatement fee of $50 for each; proof of insurance to remain on file for three years |

| Nevada | $250 to $1,000, Registration suspension — until payment of reinstatement fee and, depending on circumstances, an SR-22 (proof of financial responsibility) if lapsed more than 90 days; reinstatement fee: $250 |

| New Hampshire | Not a mandatory insurance state. Proof of insurance may be required as the result of a conviction, crash involvement, or administrative action. If you are required to file proof of insurance and vehicles are registered in your name, you will be required to file an Owner’s SR-22 Certificate of Insurance. |

| New Jersey | $300 to $1,000, License suspension for one year; pay surcharges for three years in the amount of $250 per year |

| New Mexico | Up to $300, Fine and/or imprisoned for 90 days; license suspension |

| New York | Up to $1,500 if involved in accident plus $750 civil penalty, "License and registration suspension – revoked for one year; suspension of license if without insurance for 90 days; suspension lasts as long as registration suspension; Suspension of registration: equal to time without insurance or pays $8/day up to thirty days for which financial security was not in effect, $10/day from the thirty-first to the sixtieth day $12/day from the sixtieth to the ninetieth day and proof of security is provided. Or for the same time as the motor vehicle was operated without insurance. " |

| North Carolina | $50, Registration suspension until proof of financial responsibility but 30-day suspension if in car accident or knowingly driving without insurance; $50 restoration fee plus license plate fee |

| North Dakota | Up to $1,500, "Fine and/or 30 days in prison; 14 points against license plus suspension; Proof of insurance must be provided for one year; license with a notation requiring that person keep proof of liability insurance on file with the department. The fee for this license is $50, and the fee to remove this notation is $50." |

| Ohio | License/plates/registration suspension until requirements are met and $100 reinstatement fee is paid; maintain special high-risk coverage on file with the BMV for three to five years; If involved in accident without insurance: all above penalties and a security suspension for two plus years and an indefinite judgment suspension (until all damages are satisfied) |

| Oklahoma | $250, Jail time up to 30 days; license suspension with $275 reinstatement fee. Police can seize license plates and assign temporary plates and liability insurance — in effect for 10 days and can also impound the vehicle. The cost of the temporary coverage is added to the administrative fee and any fines paid for plates to be returned. If the car isimpounded, the owner must also pay towing and storage fees. |

| Oregon | $130-$1000 ($260 is the presumptive fine), If involved in accident — at least a one year license suspension; proof of financial responsibility required for three years |

| Pennsylvania | Registration suspended for three months (unless lapse was for less than 31 days and vehicle not operated during that time); $88 restoration fee plus proof of insurance required to get it back; $500 civil penalty fee is optional in lieu of registration suspension plus $88 restoration fee — can only use this option once within a 12-month period |

| Rhode Island | $100 to $500, License and registration suspension up to three months; reinstatement fee: $30 to $50 |

| South Carolina | $100-$200, Fine or 30-day imprisonment; failure to surrender registration and plates when insurance lapses; license/registration suspended until proof of insurance plus $200 reinstatement fee |

| South Dakota | $100, Fine and/or 30 days imprisonment; license suspension for 30 days to one year; filing proof of insurance (SR-22) with the state for three years from date of conviction. Failure to file proof will result in suspension of vehicle registration, license plates, and driver license. |

| Tennessee | Pay $25 coverage failure fee within 30 days of notice; if not paid, then an additional $100 coverage failure fee with suspension or revocation of registration plus reinstatement fee of no more than $25 |

| Texas | $175 to $350, Pay up to a $250 surcharge every year for three years (may be reduced with certain requirements) |

| Utah | $400, License suspension until proof of insurance (maintained for three years) and $100 reinstatement fee |

| Vermont | Up to $500, License suspended until proof of insurance |

| Virginia | May pay $500, Uninsured Motorists Vehicle fee to drive without insurance at your own risk. If this fee is not paid in lieu of insurance, all driving and vehicle registration privileges will be suspended until a $500 statutory fee is paid, proof of insurance is filed for three years, and a reinstatement fee (if applicable) is paid |

| Washington, D.C. | Up to $250 or more |

| West Virginia | $200 to $5,000, License suspended for 30 days with reinstatement fees, unless there's proof of insurance and $200 penalty fee |

| Wisconsin | Up to $500 |

| Wyoming | Up to $750, Up to six months in jail |

If you could get backdated insurance it would be hard for authorities to identify those driving without legal insurance coverage. In short, it would make it much easier for drivers to commit fraud and to get away with driving without insurance by quickly taking out backdated policies when they needed it.

What is considered to be auto insurance fraud?

Backdating insurance in most situations is considered auto insurance fraud and you should understand what that means.

According to the FBI, insurance fraud currently costs insurance companies upwards of $40 billion dollars, which adds somewhere between $400 and $700 to the average driver’s annual insurance rates.

What should you do if there’s a gap in your auto insurance?

Some websites will allow you to backdate your auto insurance simply due to the way that they are designed. However, this is not encouraged and if you attempt to do this, you may find yourself in legal trouble.

The best thing to do then is to try and pay for the damages yourself. In order to do that, you’ll need to speak to a financial expert and possibly a lawyer to make sure you’re doing everything correctly.

You should also get an insurance policy put in place immediately, even if the company won’t backdate your coverage. A gap in your coverage will impact your rates, but once you’ve had insurance in place for a given period (typically one year), that increase will go away and you’ll be back to normal rates.

Auto Insurance Rate Increases After a Lapse In Coverage| Insurance Companies | Average Rate with No Lapse in Coverage (6 Month Rates) | Average Rate After Lapse in Coverage (6 Month Rates) | Average Rate Increase |

|---|---|---|---|

| $696.00 | $810.00 | 16.38% | |

| $730.18 | $786.88 | 7.77% | |

| $882.00 | $901.00 | 2.15% | |

| $974.82 | $1090.8 | 11.90% | |

| $651.19 | $736.52 | 13.10% |

Keep in mind that your rates are based on a variety of factors, so you can help keep your insurance costs low by keeping your commute short and maintaining a clean driving record, even if you do have a gap in your coverage.

What happens when an auto insurance policy is backdated?

In some rare instances, it’s possible to backdate your insurance coverage. Even these situations are not guaranteed, however, so do your very best to get coverage in place from the moment you purchase a vehicle.

When can you backdate coverage? What happens when an insurance policy is backdated? Let’s look at some examples of backdated auto insurance coverage.

Can you backdate coverage if you already own a policy?

So, what’s the alternative to having a gap in coverage? What are your options?

Backdating an insurance policy occurs when you purchase a new car and you already have an active insurance policy in place.

How far can you backdate auto insurance?

Typically, you have less than seven days, but sometimes as much as a month, during which your insurer will cover your vehicle. even though it hasn’t been added to your policy. Expect to be charged for the backdated time when you do add the vehicle to your policy.

Can you backdate your policy if it was terminated for non-payment?

If your auto insurance policy was canceled due to non-payment and you have had no accidents in the meantime, you might still be able to pay for the time in between and reinstate your policy.

This will prevent there from being any gaps in your coverage, but you’ll need to sign a no-loss form to state that there were no losses or accidents during the time your policy was not in place. This is usually only possible when the lapse in coverage has been less than 30 days.

How long will it take for insurance to be canceled after you stop paying your bill? It can vary, but usually between 10-30 days.

Read more: What happens if I let my auto insurance policy lapse?

Navigating the Complexities of Auto Insurance Coverage

When it comes to securing the right AAA insurance quote, it’s essential to understand the factors that can influence your rate, especially if you’ve experienced a lapse in coverage.In states like Alabama, getting a fine for an insurance lapse can be a significant financial burden.

To avoid such penalties, many drivers seek the best car insurance after a lapse in coverage options that offer affordable premiums and reliable protection. Additionally, it’s crucial to be aware of the concept of SR-22 insurance, particularly if you’ve had driving violations that require you to carry an SR-22.

For individuals who have experienced cancellation, such as when if my car insurance has been cancelled, obtaining new coverage promptly is essential. Companies like Geico offer various solutions, from Geico motorcycle insurance quotes to Geico non-owner car insurance, to cater to different needs.

Moreover, Geico provides convenient options like adding a vehicle with Geico and a reinstatement policy with Geico, simplifying the process of reactivating your insurance. For those in need of SR-22 coverage, getting SR-22 insurance from Geico is a practical approach, ensuring compliance with state requirements.

In states like Pennsylvania, it’s worth noting that in Pennsylvania an insurer may backdate coverage to prevent gaps. However, backdated insurance is generally a rare and legally complex option. For those seeking retroactive coverage, retroactive insurance coverage might be considered, but the reason for the backdating policy is often scrutinized heavily to prevent fraud.

If you’re considering reinstating a policy, insurers like Progressive and State Farm offer Progressive reinstatement policy and State Farm reinstatement policy options. Additionally, understanding the costs associated, such as the average cost of SR-22 insurance in Texas or cheap SR-22 insurance in Mississippi, is vital when managing your insurance needs.

If you’re wondering about car insurance that backdates, unfortunately, it’s generally not allowed by insurance companies due to the risk of fraud and financial instability. Attempting to obtain cheap SR-22 insurance in Indiana or any form of retroactive insurance coverage can lead to severe consequences, including legal trouble and hefty financial penalties.

While it might be tempting to seek Geico insurance quotes or explore Geico motorcycle insurance quote options after an accident, getting insurance same day as the accident is often challenging and may not be feasible.

However, there are legitimate alternatives to consider, such as Nationwide reinstatement policy options or exploring non-owner car insurance Geico for temporary coverage. Additionally, if you require SR-22 insurance in Maine or SR-22 insurance in Rhode Island filing, reputable insurers like Geico can provide assistance and guidance.

It’s essential to prioritize maintaining active coverage and obtaining proof of coverage promptly to avoid gaps and ensure compliance with state requirements.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Navigating Specific Insurance Scenarios and Coverage Options

In the realm of auto insurance, there are various specific scenarios and coverage options that drivers might encounter. Understanding these unique situations can help you make informed decisions about your insurance policy and ensure you maintain continuous coverage.

Geico Backdated Insurance and Policy Reinstatement

When considering Geico backdated insurance, it’s essential to understand that most insurance companies, including Geico, do not permit backdating policies. If you need to reinstate your insurance, it’s crucial to act promptly to avoid lapses and additional fees.

Situations Requiring Backdated Car Insurance

There are instances where drivers feel they need backdated car insurance. This typically arises if there’s been a lapse in coverage, and the driver wants to avoid penalties or higher premiums. However, it’s important to note that backdating is generally not allowed and can be considered fraudulent.

Liberty Mutual Backdated Cancellations

For those insured with Liberty Mutual, the concept of backdate cancellation Liberty Mutual or backdate cancellations Liberty Mutual might seem appealing if a policy was inadvertently canceled. Unfortunately, Liberty Mutual, like most insurers, does not typically allow backdating cancellations due to the legal and financial risks involved.

Age-Based Backdating and Coverage Gaps

Some drivers may wish to backdate to save age, particularly if younger drivers believe they can benefit from lower premiums. This practice is rare and often not permitted by insurers. Instead, maintaining continuous coverage is the best strategy to manage premiums effectively.

Finding Car Insurance That Backdates

While searching for car insurance that backdates might be tempting, it is largely impractical. Most insurance companies do not offer backdated policies due to the risk of fraud. Instead, drivers should focus on securing immediate coverage to avoid gaps.

Affordable Solutions for Lapsed Coverage

If your coverage has lapsed, finding cheap auto insurance lapsed coverage is essential. Some insurers specialize in providing coverage for those who have experienced lapses. Researching and comparing options can help you find the best car insurance for lapsed coverage to minimize financial impact.

Progressive Auto Insurance and Short-Term Coverage

Exploring options with well-known companies like Progressive Auto Insurance can provide insights into managing lapses and reinstating coverage. Additionally, temporary solutions such as temporary car insurance in Michigan can offer short-term protection while you secure a long-term policy.

Specific Policy Considerations

Understanding how to reinstate car insurance and the implications of car insurance reinstatement fees is crucial for drivers who have had their policies canceled. This can help in planning financially and avoiding further penalties.

Legal Aspects and Car Insurance Payback

Drivers often wonder will car insurance backdates or how car insurance payback works. Generally, backdating is not allowed, but knowing the legal implications and alternatives can help manage expectations and avoid fraud.

Navigating State-Specific Laws

State regulations, such as New Hampshire auto insurance laws, can significantly impact your insurance coverage and requirements. Staying informed about your state’s laws can help ensure compliance and continuous coverage.

Comparing Insurance Quotes

Obtaining a Geico car insurance quote and comparing it with other insurers can help you find the best rates and coverage options. Utilizing quotes effectively can aid in preventing future lapses and securing the right policy for your needs.

Understanding Retroactive Coverage

While retro car insurance or car insurance that backdates might seem like viable solutions, they are rarely feasible. Ensuring you have continuous, legitimate coverage is the best way to protect yourself legally and financially.

By understanding these specific scenarios and coverage options, drivers can navigate the complexities of auto insurance more effectively, ensuring they remain protected and compliant with state laws and insurance requirements.

What does backdated liability insurance typically cover?

Realistically, nothing is covered by backdated auto liability insurance. The purpose of backdating a policy is generally just to prevent a gap in coverage.

In fact, most insurance companies will require you to sign a no-loss form guaranteeing that you had no accidents or other claims during the time in which you want your coverage backdated.

What is uninsured/underinsured motorist coverage?

Uninsured/underinsured motorist coverage often referred to as UM, is a coverage you can buy to protect yourself in the event that you’re hit by a driver who has no insurance or only carries the minimum insurance required by law.

It’s a way to protect yourself financially, but don’t assume that it’s a perfect solution. Insurance companies will fight vigorously to prevent paying out on a UM claim and drivers who cause accidents while uninsured should know that an insurance company can sue you to recoup costs that it paid out on UM coverage.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Backdated Auto Insurance: The Bottom Line

Backdated auto insurance, sometimes referred to as retroactive car insurance, is not impossible, but it’s incredibly unlikely and will never pay for bodily injury or property damage insurance claims caused while you were uninsured.

Avoid the need to backdate your auto insurance by making sure you have the right insurance plan for you. Get started by entering your ZIP code into our free tool to get car insurance quotes without having to backdate your auto insurance.

Frequently Asked Questions

Can I backdate my auto insurance coverage?

Backdating auto insurance coverage is generally not allowed by insurance companies. Backdating coverage after an accident or incident is not possible and may be considered fraud, leading to criminal penalties. It’s important to maintain continuous car insurance coverage to avoid legal and financial consequences.

Why won’t auto insurance companies backdate policies?

Auto insurance companies calculate rates carefully to ensure they make a profit. Allowing backdated policies would result in increased claims for the company, leading to financial losses. Insurance companies aim to provide coverage from the policy’s start date and typically do not allow backdating.

What should I do if there’s a gap in my auto insurance coverage?

If you have a gap in your auto insurance coverage, it’s important to rectify it as soon as possible. You should contact an insurance provider and obtain coverage immediately. While the gap may impact your rates, maintaining continuous coverage will help mitigate any long-term consequences.

Can uninsured motorist coverage protect me if I have an accident with an uninsured driver?

Uninsured/underinsured motorist coverage (UM/UIM) can provide financial protection if you’re involved in an accident with a driver who doesn’t have insurance or carries insufficient coverage. However, it’s important to note that insurance companies may contest UM/UIM claims, and uninsured drivers can be held personally responsible for the costs incurred by the insurance company.

What are the legal issues with backdated auto insurance?

Backdating auto insurance is generally considered fraud and can have legal consequences. Insurance companies and authorities aim to prevent fraudulent activities and ensure drivers maintain continuous coverage. Backdating insurance policies can make it easier for drivers to commit fraud and avoid legal requirements, leading to increased risks and costs for insurance companies and the general public.

What is a No Known Loss Letter for retroactive auto insurance?

It’s the no-loss form we mentioned earlier, which indicates that there were no losses or accidents during the time your policy lapsed. Typically, this form of backdating is only available if your lapse in coverage was less than 30 days.

Can auto insurance be reinstated after cancellation?

Yes, auto insurance can often be reinstated after cancellation, but it typically depends on the insurer’s policies and the length of the lapse in coverage.

Can an insurance company backdate a policy?

Generally, insurance companies do not backdate policies due to the risk of fraud and financial losses.

Can car insurance companies backdate policies?

No, car insurance companies usually do not backdate policies as it can lead to fraudulent claims and financial instability.

Can force-placed insurance be backdated?

Force-placed insurance is typically backdated to the date of the lapse to ensure continuous coverage, but this practice varies by lender.

Can health insurance be backdated?

Can I backdate the car insurance?

Can I purchase insurance and backdate it to cover an accident?

Can insurance backdate coverage?

Can the insurance company backdate the policy?

Can insurance be backdated?

Can you backdate car insurance coverage?

Can you backdate the insurance?

Can you backdate an insurance policy?

Can you backdate the insurance cancellation?

Can you backdate insurance coverage?

How far back can an insurance company audit?

How many years do insurance companies go back?

How to backdate car insurance?

How to backdate insurance?

How to get backdated car insurance?

Is backdating insurance illegal?

What car insurance companies will backdate insurance?

What does backdate mean?

What happens when an insurance policy is backdated?

What insurance companies go back 3 years?

What insurance companies will backdate car insurance?

What insurance companies will backdate insurance?

What is backdating in insurance?

How to get auto insurance after a lapse in coverage?

How to reinstate canceled auto insurance?

Can you get retroactive car insurance?

Can a lapsed car insurance policy be reinstated?

Can car insurance be backdated?

Can car insurance be reinstated?

Can car insurance be retroactive?

Can I reinstate my car insurance?

Can insurance companies backdate policies?

Can you buy retroactive car insurance?

Can you reinstate a canceled car insurance policy?

Can you reinstate a canceled car insurance policy with Progressive?

Can you reinstate your car insurance?

Can you start car insurance same day?

How long can I wait to file a car insurance claim?

How long do you have to add a new car to your Geico insurance policy?

How to get car insurance after lapse?

Will insurance backdate?

Can you get your car insurance backdated?

Related Articles

-

Mar 2025

What happens if I disagree with Progressive’s decision on my auto insurance claim?

-

Dec 2024

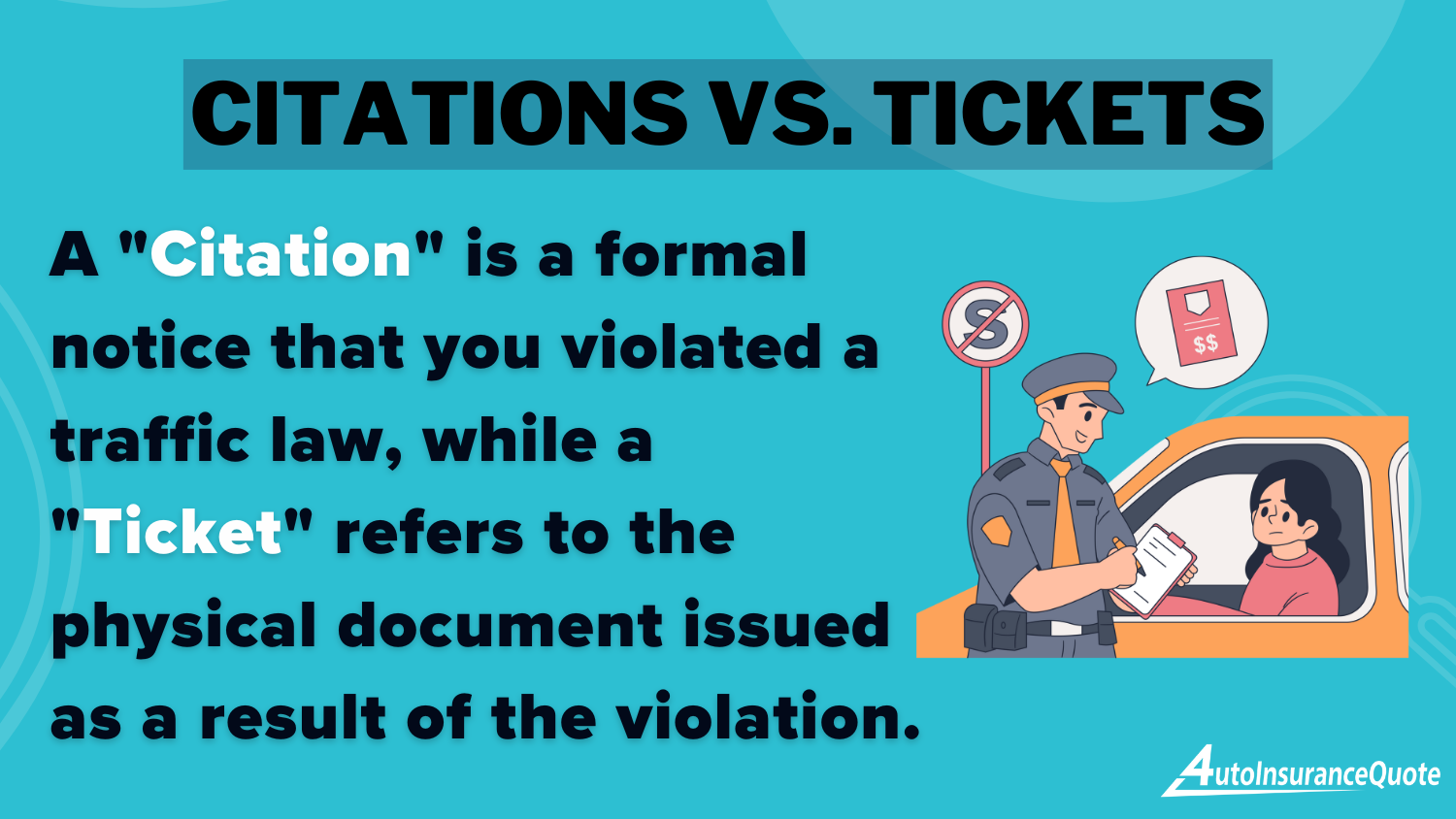

Citations vs. Tickets in 2026 (Differences Explained)

-

Nov 2024

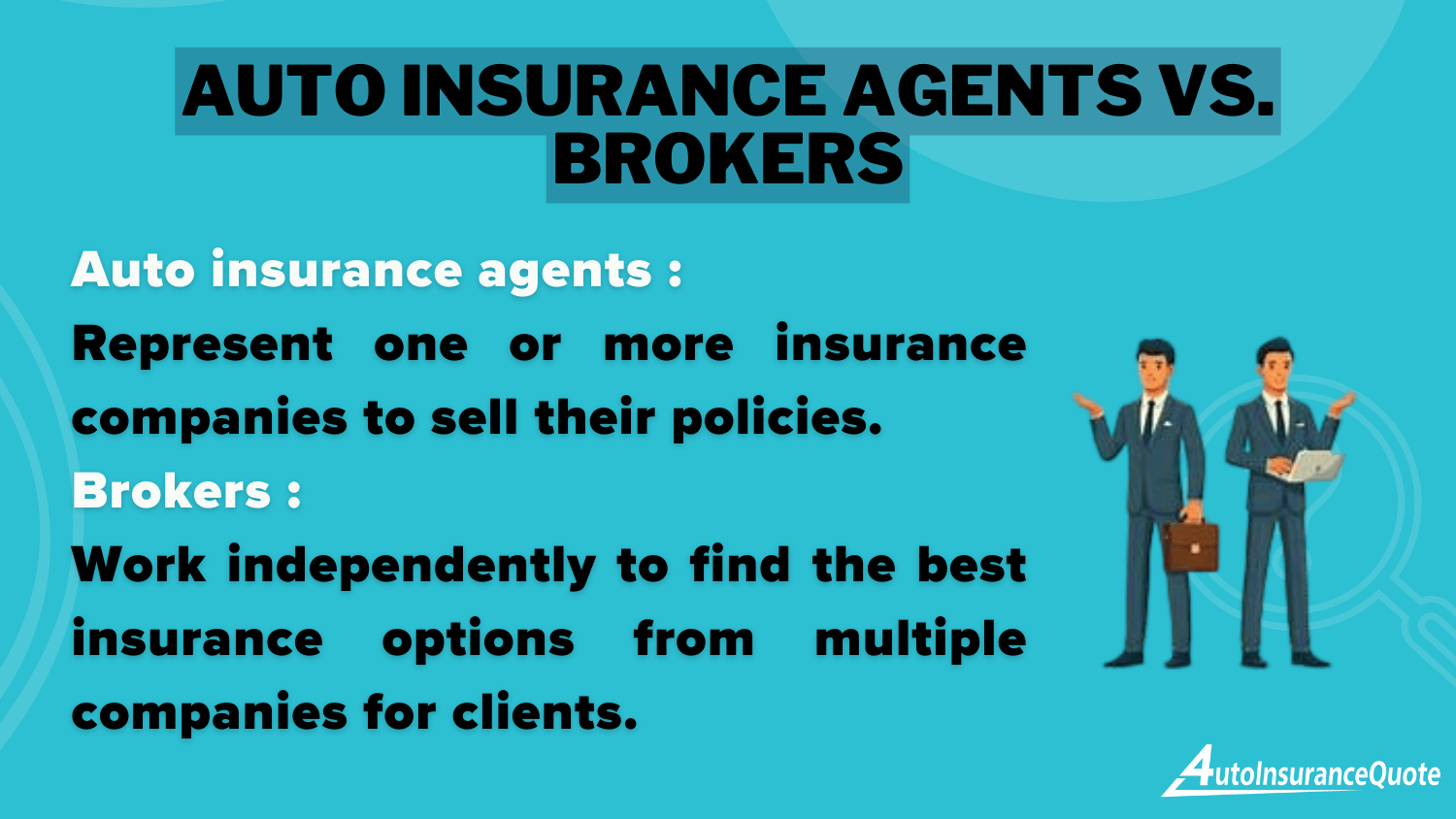

Auto Insurance Agents vs. Brokers in 2026 (Differences Explained)

-

Mar 2025

Are you required to add your children to your auto insurance policy?

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption